“Should I raise under Reg D or Reg A?”

It’s one of the most common questions in private markets, and one of the most misleading.

Because most capital raises don’t stall due to choosing the wrong exemption. They stall because the system behind the raise wasn’t designed to scale.

Reg D works until your network runs out.

Reg A expands access but introduces complexity most capital raisers underestimate.

So, the real question isn’t which structure to choose.

It’s what actually breaks as you try to grow, and whether your setup can handle it.

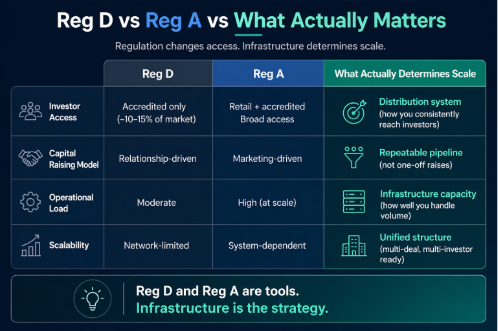

Reg D vs Reg A Explained: What They Do (and Where They Break)

At a surface level, the distinction is straightforward.

Reg D (506(b) and 506(c)) allows you to raise primarily from accredited investors. 506(c) is accredited-investor-only, while 506(b) can include up to 35 non-accredited but sophisticated investors, subject to restrictions. In practice, that’s still a limited pool; roughly 10–15% of the population.

Capital raising here is relationship-driven: warm intros, existing LPs, direct conversations. It’s efficient. It’s familiar. And it works: early.

Reg A, by contrast, opens the door much wider.

It allows you to raise from both accredited and non-accredited investors, effectively unlocking mass participation. But that access comes with trade-offs: higher compliance requirements, ongoing reporting, and a fundamental shift in how capital is raised.

You move from conversations to systems. Here’s the part most people miss:

- Reg D is optimized for relationships

- Reg A is optimized for scale

But neither one builds the system required to support either, and that’s where things start to break.

The First Constraint: Distribution Limits (Where Reg D Caps Out)

Reg D doesn’t fail; it saturates. In the early stages, most managers raise capital from:

- Personal networks

- Existing relationships

- Referrals and introductions

That’s often enough to:

- Close initial deals

- Build early traction

- Establish credibility

But over time, that early momentum runs out. The same investors:

- Get allocated elsewhere

- Become more selective

- Experience “deal fatigue”

At the same time:

- More managers enter the market

- Competition for accredited capital increases

- LP expectations rise

This creates a distribution ceiling. Not because demand disappears, but because:

your access to new capital doesn’t expand at the same rate as your ambition.

This is where many capital raisers misdiagnose the issue. They assume:

- The deal isn’t strong enough

- The market has slowed

- Investors aren’t interested

When in reality: They’ve simply exhausted their reachable audience.

The Second Constraint: Operational Complexity as You Scale

Let’s assume you solve for distribution. Now a different problem shows up.

As your capital raised increases, so does:

- The number of investors

- The frequency of communication

- The volume of reporting

- The complexity of compliance

- What worked with 20 investors doesn’t work with 200 investors

This is where operational friction starts compounding:

- Investor onboarding becomes slower

- Documents need constant coordination

- Updates become inconsistent

- Reporting becomes fragmented

- Tax handling (K-1s, filings) becomes burdensome

At this stage, capital raising doesn’t slow down because of demand. It slows down because your system can’t process the volume efficiently.

This is the hidden reality of scale: Raising more capital is easy compared to managing it well.

The Third Constraint: Fragmented Structures Break at Scale

Most managers don’t operate within a unified system. Instead, they build:

- One SPV per deal

- Separate structures over time

- Multiple disconnected processes

This works early. But as deals increase, fragmentation compounds:

- Each raise requires new setup

- Each investor has a different experience

- Data lives in multiple systems

- Reporting becomes inconsistent

The result: You’re not scaling a system; you’re managing a collection of isolated transactions.

This Creates Three Major Problems:

- Operational duplication: Every deal resets the process

- Investor friction: Repeated onboarding, inconsistent experience

- Inability to scale across deals: No continuity in capital or relationships

This is where most capital raising models quietly break.

Why Reg A Doesn’t Solve These Problems (On Its Own)

At this point, many capital raisers look at Reg A as the solution, and on paper, it makes sense:

- Larger investor pool

- Broader access

- Potential for scale

But Reg A introduces a different kind of challenge. It shifts capital raising from:

- Relationship-driven → marketing-driven

Now success depends on:

- Lead generation systems

- Funnel optimization

- Conversion rates

- Investor education at scale

At the same time:

- Investor volume increases significantly

- Communication demands multiply

- Operational complexity expands

So instead of solving your constraints, Reg A does something else: it amplifies them.

If your system isn’t built for scale, Reg A won’t fix your capital raising. It will expose what’s broken.

The Real Limiter: Infrastructure, Not Regulation

Across both Reg D and Reg A, the pattern is consistent: managers don’t fail because of:

- The wrong exemption

- Lack of investor interest

They fail because:

- Their distribution doesn’t scale

- Their operations don’t scale

- Their structure doesn’t scale

This is why the Reg D vs Reg A debate is incomplete. It focuses on access, not capability. The real question is: Can your system handle growth once it starts?

Because capital raising in 2026 is no longer about: finding investors.

It’s about:

- Supporting them

- Managing them

- Scaling with them

What Scalable Capital Raising Looks Like in 2026

The capital raisers who are still scaling today have made a shift. They’re no longer thinking in:

- Deals

- Individual raises

- Isolated structures

They’re thinking in systems and that system includes:

- A unified structure across multiple investments

- The ability to raise across different investor types

- Centralized investor management

- Consistent onboarding and reporting

- Infrastructure that supports both Reg D and Reg A

Instead of rebuilding for every raise, they operate within a framework that:

- Compounds investor relationships

- Supports repeat participation

- Reduces operational friction

- Enables consistent capital flow

Where Avestor Fits?

This is where platforms like Avestor change the equation. Instead of forcing managers to:

- Choose between structures

- Rebuild infrastructure every time

Avestor provides a unified framework that supports:

- Multi-deal capital raising

- Multiple investor types

- Regulatory flexibility across Reg D and Reg A, depending on the offering, structure, and legal requirements

- Integrated investor management, compliance, and reporting

The result? Managers don’t just raise capital. They build systems that keep capital moving. The industry spends too much time asking, “Should I use Reg D or Reg A?”

But that’s not what determines whether you scale.

Reg D will get you started.

Reg A can expand your reach.

But neither will fix a system that wasn’t built for growth, because in 2026, capital raising doesn’t break at the regulatory level. It breaks at the structural level and the managers who win aren’t the ones who pick the right exemption. They’re the ones who build infrastructure that doesn’t break, no matter how far they scale.

Reg D vs Reg A: Frequently Asked Questions

- What is the main difference between Reg D and Reg A?

Reg D limits capital raising primarily to accredited investors, while Reg A allows both accredited and non-accredited investors to participate, with additional compliance requirements.

- Is Reg A better than Reg D?

Not necessarily. Reg A provides broader access to investors, but also introduces more complexity, cost, and operational requirements. The better option depends on your strategy and infrastructure.

- Can you use both Reg D and Reg A?

Yes, depending on how your fund is structured and how offerings are organized, fund managers may use different exemptions across different raises.

- Why do most fund managers start with Reg D?

Reg D is faster to execute, requires less regulatory overhead, and works well for relationship-driven capital raising.

If you’re thinking about moving beyond your current structure or trying to understand what scaling capital requires, it helps to look at your setup from a systems perspective. That’s a conversation we have with fund managers every day.

👉 If you want to explore that, you can book time here: https://www.avestorinc.com/video