If you were starting a business, you would not only ask what it costs to set up.

You would ask what the business can create.

Fund managers should think about structure the same way. The first question is often:

“What does it cost to launch?”

That matters. But it is not the full question. The better question is:

“What income model can this structure help support?”

A Customizable Fund® is not just a way to raise capital. It is an infrastructure for building a fund business. And like any business infrastructure, its value should be measured against the opportunity it helps create.

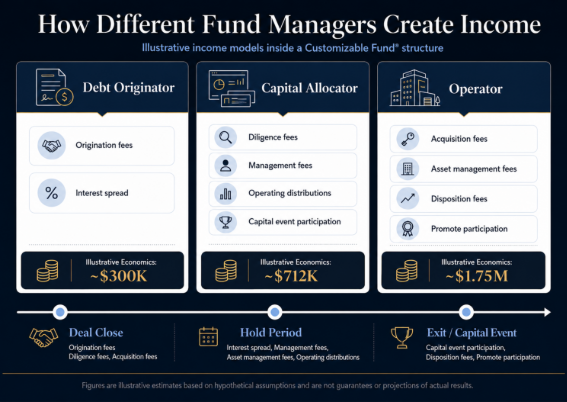

How Fund Structure Supports Manager Income

Not every fund manager earns the same way.

Debt originators, capital allocators, and operators each create value differently. So, the structure should support the economics behind that role.

A fund structure should not only help money move into deals. It should support how income is created across the life of those deals. That income may show up through:

- Fees at deal close

- Management income during the hold period

- Interest spread or operating distributions

- Disposition fees, capital events, or promote at exit

For some managers, that may mean origination fees or interest spread.

For others, it may mean diligence fees, management fees, operating distributions, or participation in capital events.

For operators, it may include acquisition fees, asset management fees, disposition fees, and promote.

The structure matters because the income model matters.

Customizable Fund® Income Models for Different Fund Managers

The following examples are illustrative only. They are based on hypothetical Customizable Fund® models and assumptions, not guaranteed or projected results.

But they show the real point: The income model changes depending on the role the manager plays.

Debt Originator Income Model

For a debt originator, the model is relatively direct.

The manager may earn when loans are originated and may also earn through interest spread during the hold period.

In one illustrative model based on $5 million raised, the assumptions included:

- 10 loans

- $500,000 per loan

- 2% origination fee

- 2% interest spread over 24 months

That created approximately:

- $100,000 from origination fees

- $200,000 from interest spread

Total illustrative economics: approximately $300,000.

This is not an operator model.

There is no acquisition fee, disposition fee, or promote. The income comes from originating debt and capturing spread.

That is the business.

The structure should support that.

Capital Allocator Income Model

Capital allocators are different.

They may not operate the asset directly, but they still create value by:

- Sourcing opportunities

- Evaluating sponsors

- Performing diligence

- Managing investor relationships

- Allocating capital into deals that fit the strategy

That work can also support economics.

In one illustrative model based on $5 million raised, the assumptions included:

- 10 deals

- $500,000 allocated per deal

- 2% diligence fees

- 1% management fees over 5 years

- 10% of operating distributions

- 10% participation in capital events

That created approximately:

- $100,000 from diligence fees

- $245,000 from management fees

- $220,000 from operating distributions

- $147,000 from capital event participation

Total illustrative economics: approximately $712,000.

This distinction matters.

Capital allocators are not simply “raising money for someone else’s deal.”

If structured properly, the allocator role can create economics around sourcing, diligence, management, distributions, and capital events. That is a different business model than direct asset operation, but it is still a business model.

Operator Income Model

Operators usually have the broadest income stack because they are closest to the asset.

They are involved in:

- Acquisition

- Execution

- Business plan management

- Final outcome

So, their economics may appear across the full lifecycle of the deal.

In one illustrative model based on $5 million raised, the assumptions included:

- 5 deals

- $1 million raised per deal

- $3 million purchase price per deal

- 2% acquisition fee

- 1% annual asset management fee

- 2% disposition fee

- 30% promote at a 2x equity multiple

That created approximately:

- $300,000 from acquisition fees

- $250,000 from asset management fees

- $300,000 from disposition fees

- $900,000 from promote participation

Total illustrative economics: approximately $1.75 million.

That number is not the point by itself. The point is what creates it.

The operator model can generate economics at acquisition, during management, and at exit. The fund is not just collecting capital. It is supporting the business model behind the manager’s execution.

Why Fund Setup Cost Is the Wrong Starting Point

Every business has startup costs.

A fund is no different.

Legal, platform, administrative, and operational costs are real. But they are only one side of the equation.

Looking at cost without understanding the income model is incomplete.

A manager building a one-time transaction may evaluate structure one way. A manager building a repeatable capital business has to evaluate it differently.

The better question is not simply: What does this cost?

The better question is: Can this structure support how I earn and scale over time?

That is the real evaluation.

The structure is not separate from the economics. It is what allows those economics to be organized, supported, and repeated.

How Avestor Helps Fund Managers Build Scalable Fund Infrastructure

This is where Avestor’s Customizable Fund® model fits differently.

Not simply as software.

Not just as a way to launch a fund.

But as infrastructure for building a capital business around the way a manager actually earns.

The role may differ. The principle does not.

The fund structure should match the opportunity the manager is building.

That is why the conversation should not begin and end with the set-up cost. It should begin with the business:

- What are you building?

- How do you create value?

- Where does income come from?

- What structure can support that over time?

If you need help building out the opportunity, that is where Avestor can help. Schedule a 15-minute discovery call, and our team will connect with you based on your availability.

____________________________________________________________________________________

Disclaimer: The examples and figures above are illustrative estimates only based on hypothetical assumptions and do not represent guarantees, projections, or actual results. Outcomes vary based on fund structure, strategy, execution, market conditions, fees, expenses, investor terms, and other factors. Avestor does not provide legal, tax, investment, or financial advice.