Most fund managers ask the wrong question first.

They ask: “Can I market this offering?”

That question matters. But it is not where the decision should start.

The better question is: “How am I actually planning to raise capital?”

That is where the real difference between Rule 506(b) and Rule 506(c) begins.

On paper, both are exemptions under Regulation D. Both can be used by private companies and fund sponsors to raise capital without conducting a fully registered securities offering. Both can support unlimited raise amounts when the applicable requirements are met.

But for fund managers, the choice is not just a technical compliance decision. It changes the entire fundraising motion.

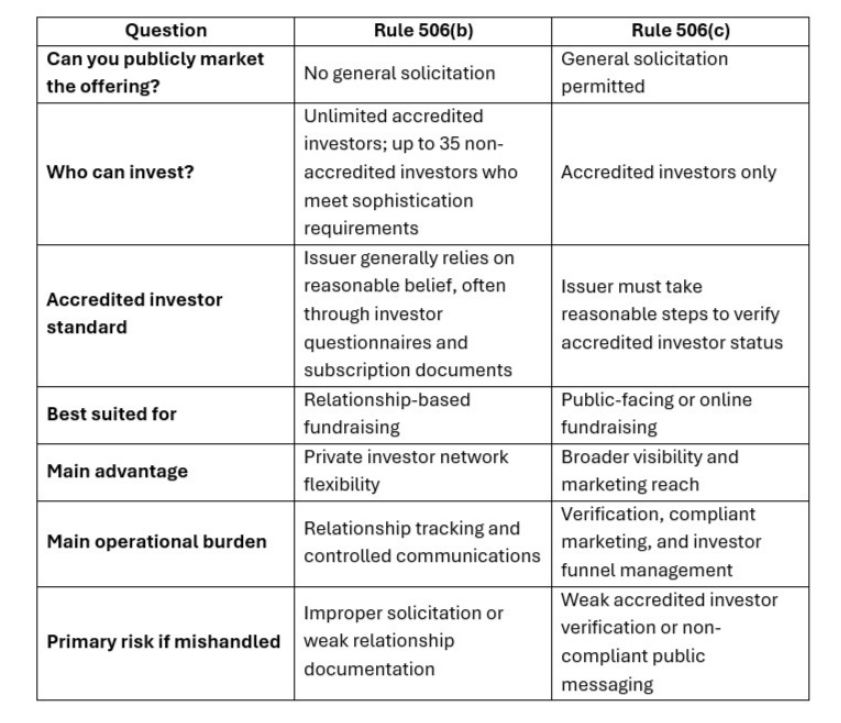

Rule 506(b) is generally built around private, relationship-based capital raising where general solicitation is not permitted.

Rule 506(c) permits a more public-facing fundraising strategy because general solicitation is allowed when the required conditions are met.

Neither is automatically better.

The right choice depends on the investor strategy, marketing motion, verification process, and operational infrastructure the manager is prepared to support.

Why Rule 506 Matters for Private Fund Managers?

Regulation D remains one of the most important frameworks for private capital formation in the United States.

According to SEC Regulation D offering statistics, there were 34,553 initial Reg D filings in 2025, representing approximately $2.39 trillion in total reported amount sold. Fund issuers represented a major share of that market, with roughly $2.12 trillion in reported amount sold by fund issuers.

Rule 506 is especially important because it allows companies relying on the exemption to raise an unlimited amount of money, subject to the applicable requirements.

But the data also shows something important: Rule 506(b) remains far more commonly used than Rule 506(c).

In 2025, SEC data showed:

- 30,315 Rule 506(b) offerings

- 3,989 Rule 506(c) offerings

That does not mean 506(b) is always better. It means many issuers still default to private, relationship-based fundraising even though 506(c) permits broader public marketing.

For fund managers, that makes the decision more strategic.

The question is usually not whether Rule 506 can support the size of the raise. In many cases, it can. The real question is whether the exemption supports the way the manager plans to raise.

A manager raising quietly from a known investor network has a very different fundraising motion than a manager building a public content engine, running webinars, publishing deal education, or driving online traffic to an offering.

That difference is where 506(b) and 506(c) start to separate.

What Is Rule 506(b)?

Rule 506(b) is the traditional private placement path.

It generally allows issuers to raise an unlimited amount of capital and sell securities to an unlimited number of accredited investors. It may also allow sales to up to 35 non-accredited investors, provided those investors meet sophistication requirements, and the issuer satisfies additional disclosure obligations.

But there is one major constraint: No general solicitation.

That means no broad public advertising, no public promotion of the offering, and no general marketing campaign designed to solicit investors into that specific raise.

In practice, 506(b) often depends on private, relationship-based fundraising because general solicitation is not permitted.

For many sponsors, that is still the right fit.

If a manager already has a strong investor network, existing relationships, referral channels, and private communication workflows, 506(b) may align well with how they actually raise.

But it also creates a real limitation.

If the manager does not already have enough investor relationships, 506(b) can become difficult. The sponsor cannot simply post the offering publicly, run ads, promote the deal broadly, or use public content to solicit investors into that specific raise.

That means the backend of a 506(b) raise needs to be disciplined in a different way.

Managers need to know:

- Who they already have a relationship with

- How investor conversations are being tracked

- Who has access to offering materials

- What communications have been sent

- Whether the process remains appropriately private

Managers should also remember that Rule 506 offerings generally require a Form D filing within 15 calendar days after the first sale. Rule 506 offerings are federally preempted from state registration and qualification requirements, but state notice filings and fees may still apply.

For 506(b), the fundraising engine is not public attention. It is investor relationship management.

What Is Rule 506(c)?

Rule 506(c) permits general solicitation.

Under Rule 506(c), issuers may broadly solicit and generally advertise an offering, provided that all purchasers are accredited investors, the issuer takes reasonable steps to verify accredited investor status, and the other conditions of Regulation D are satisfied.

That means fund managers using 506(c) may generally market more publicly.

They may be able to discuss the offering in public channels, build awareness through content, promote the opportunity online, or reach investors outside their existing private network.

That can be powerful. But it comes with a different burden.

Under 506(c), all purchasers must be accredited investors, and the issuer must take reasonable steps to verify that status. This is different from relying only on standard investor self-certification.

That verification requirement changes the operating model.

A 506(c) raise is not just “506(b) with marketing.”

It requires the infrastructure to handle a more public funnel.

Managers need to think about:

- Investor education before the offering

- Public-facing messaging

- Accredited investor verification

- Subscription workflows

- Follow-up systems

- Documentation

- Compliance review of marketing materials

Purchasers in Rule 506 offerings generally receive restricted securities. Rule 506(c) offerings also generally require a Form D filing within 15 calendar days after the first sale, and state notice filings and fees may still apply.

Public visibility can create more reach. It can also expose weak infrastructure faster.

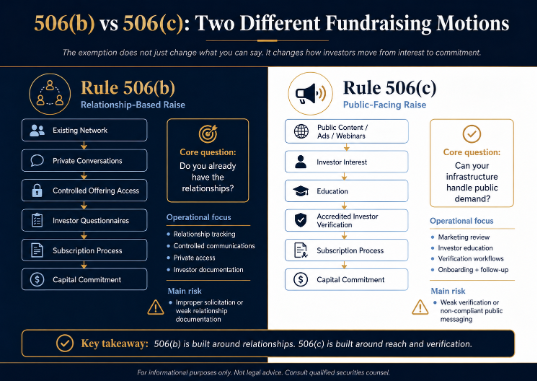

506(b) vs 506(c): The Real Difference Is the Fundraising Motion

The most common way to compare 506(b) and 506(c) is by listing the rules.

That is useful. But it is not enough.

The more important distinction for fund managers is the fundraising motion each exemption supports.

This is the real difference:

506(b) asks: Do you already have the relationships?

506(c) asks: Can your infrastructure handle public demand?

That is why managers should not choose based only on which rule sounds more flexible. They should choose based on how they actually plan to raise.

When 506(b) May Make More Sense

Rule 506(b) may make more sense when the fundraising strategy is relationship-driven.

This usually applies when a manager already has a warm investor network, referral relationships, prior investors, or an existing community where trust has been built over time.

506(b) can work well when:

- The manager does not need public marketing to fill the raise

- The investor base is already known

- The offering is shared privately

- Relationship history is important to the raise

- The sponsor prefers a quieter capital raising process

- The manager has strong CRM and investor communication discipline

But managers should not confuse private with easy.

A 506(b) raise still requires process.

If investor conversations are scattered across inboxes, texts, spreadsheets, calls, and informal introductions, the manager may struggle to maintain control as the raise grows.

The offering may be private, but the operations still need to be organized.

That is where many smaller sponsors underestimate the work.

The fund structure is one part of the raise.

The investor relationship system is another.

When 506(c) May Make More Sense

Rule 506(c) may make more sense when the manager wants to raise through a public-facing strategy.

That may include online content, webinars, paid media, public deal education, social media, podcast appearances, public-facing landing pages, or other forms of broader investor outreach.

506(c) can be a stronger fit when:

- The manager wants to publicly discuss the offering

- The investor audience is expected to be accredited only

- The sponsor has a content or audience-building strategy

- The raise depends on reaching investors beyond an existing network

- The manager is prepared to verify accredited investor status

- The backend can support higher investor volume

But 506(c) is not automatically better because it allows marketing.

Marketing creates attention.

It does not automatically create trust. It also does not replace investor education, verification, onboarding, documentation, and follow-up.

This is where many managers get the sequence wrong. They think the hard part is getting more visibility.

But 506(c) is only valuable if the manager has a system to convert public attention into verified, properly onboarded investors.

A public raise needs more than an audience.

It needs a system.

The Online Capital Raising Mistake Fund Managers Make

The biggest mistake managers make with online capital raising is assuming that traffic is the same thing as a capital raising strategy.

It is not.

Public attention is only the top of the funnel.

What happens after someone clicks matters more.

Can the investor understand the opportunity? Can they verify whether they are eligible? Can they move through the onboarding process cleanly? Can the manager follow up without losing track of conversations? Can the sponsor explain the structure, risks, fees, liquidity, and investor experience clearly?

These questions matter because online capital raising increases the number of touchpoints.

More visibility means more inquiries.

More inquiries mean more education.

More education means more documentation.

More documentation means more need for process.

That is why the exemption decision cannot be separated from the operating model.

This is also why scalable capital raising depends on more than structure alone; it requires connected systems across onboarding, compliance, investor communication, and operations, which we explore further in Start Scaling with Avestor’s 6 Pillars of Growth.

A manager choosing 506(c) because they want to market publicly also has to ask whether they are ready to handle the operational consequences of public interest.

The same is true for 506(b).

A manager choosing 506(b) because they want a private raise still has to ask whether their investor relationship process is strong enough to support the raise without public solicitation.

Different exemptions.

Different fundraising motions.

Different infrastructure requirements.

How To Decide Between 506(b) and 506(c)

The better way to evaluate 506(b) vs 506(c) is not to ask which exemption is “better.”

The better question is which exemption supports the capital raising system you are actually building.

Fund managers should work with qualified securities counsel when selecting an exemption. But from a business strategy perspective, these are the questions worth answering early.

Investor Strategy

- Do you already have enough investor relationships to support the raise?

- Do you need to publicly discuss the offering to create demand?

- Is your raise relationship-driven or audience-driven?

Eligibility and Compliance

- Are all expected investors accredited?

- Are you prepared to verify accredited investor status if required?

- Have counsel and compliance reviewers evaluated your planned communications?

Operations

- Do you have investor education materials ready before the raise opens?

- Can your onboarding process handle increased investor volume?

- Is this a one-off raise or a repeatable capital platform?

That last question is especially important.

A one-off raise can sometimes survive with more manual process.

A repeatable capital platform cannot.

If the goal is to raise repeatedly, bring investors into multiple opportunities, or build a long-term fund business, then the exemption decision should be evaluated alongside the infrastructure needed to support it.

The rule determines what is permitted. The operating model determines what is practical.

Where Avestor Fits

Avestor does not replace securities counsel, and it does not decide which exemption a sponsor should use.

That decision should be made with qualified legal advisors.

For a deeper look at how Avestor approaches Regulation D exemptions, legal documentation, and compliance support inside the Customizable Fund® model, read Customizable Fund® and Compliance: How Avestor Does It.

But once the manager understands the strategy, the next question is execution.

How will investors be onboarded? How will offering materials be organized? How will investor interest be tracked? How will communications be managed? How will participation be structured across opportunities? How will the manager avoid rebuilding the backend every time they raise?

That is where infrastructure becomes important.

Avestor’s Customizable Fund® model is designed for managers who want to build a more scalable capital raising system around the way they actually operate.

For some managers, that may be a private, relationship-driven strategy.

For others, it may involve a more public-facing investor education and marketing motion.

Either way, the principle is the same:

The exemption determines what kind of raise you can run. The infrastructure determines whether you can run it professionally.

The Exemption Is Not the Strategy

506(b) and 506(c) are both useful.

But neither one is a strategy by itself.

506(b) does not solve the problem of weak investor relationships.

506(c) does not solve the problem of weak investor trust.

The real work is deciding how the manager intends to raise, who they intend to reach, what kind of investor experience they want to create, and what infrastructure is needed to support that process.

Fund managers should not begin with the rule.

They should begin with the model.

What are you building?

Who are you trying to reach?

How will those investors move from interest to commitment?

And can your infrastructure support that journey professionally?

That is the question that matters.

If you are planning a Reg D raise and need help thinking through the infrastructure behind your capital raising strategy, Avestor can help you build the model around it.