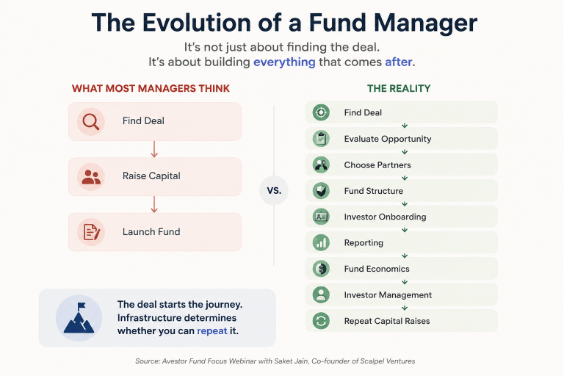

Six years ago, Saket Jain would have said finding the deal was the hard part. Not anymore.

Jain co-founded Scalpel Ventures, which invests at the intersection of syndication, venture capital, and orthopedic implants. He has spent sixteen years investing in the space and three years running a formal fund. He made that point in a recent Avestor Fund Focus webinar, in conversation with Avestor co-founder Badri Malynur.

Sourcing a deal, he told Badri, while still difficult is also the easiest part.

What's hard is everything after: how you evaluate it, who you run it with, your reporting cadence, keeping the fund funded between raises, and whether the structure exists before the opportunity does.

Most managers build in the opposite order: find the deal, excite investors, then build the entity, documents, and reporting under pressure. Working with Avestor, Scalpel took two months to build its structure before its first deal existed. That deal closed within a month of the structure being ready.

Reversed, Jain says, they'd have missed an opportunity now tracking toward a public listing at an estimated 20x. That's not an argument for planning ahead in theory. It's a dollar figure attached to getting the sequence backwards.

Here's how Jain built the structure that made that possible, and why he'd rather turn away a check than take the wrong one (more on the investor who almost walked, then wrote $700,000, further down).

Syndication or Blind Pool: Why Are You Choosing At All?

Before the fund, Jain raised money the way most capital raisers do, deal by deal, informally. It paid him nothing: no promote, no carry, no fee, just free labor repeated.

The alternative, the blind pool, asks investors to lock up capital for years and trust the manager's judgment. Jain didn't want that either: "I really like the model of syndication, where the investor is empowered" to evaluate a specific deal and decide.

But pure syndication has its own tax: a new entity and documents for every deal, $10,000 to $25,000 in legal cost each time, brutal math against $250,000 to $3 million raises.

Scalpel's structure, built on Avestor's Customizable Fund® model , holds both models at once: one legal setup, signed once, plus a short deal-specific document for each opportunity an investor chooses. "It's basically syndication, powered by a platform," Jain tells investors.

The pitch isn't just returns. It's never having to find another platform again.

Learn more about the Customizable Fund® model and how it offers a middle path between blind pools and one-off syndications by combining deal-level investor choice with a longer-term fund structure.

Why Should Investors Trust You Over the Next Manager?

Scalpel's structure only works because of something that predates it by a decade: a genuinely narrow specialization.

Jain's partner is an orthopedic surgeon. Implant design hasn't changed much since the 1930s. Roughly 25% of Americans are allergic to nickel; nearly all metal implants use it. A predictable share are built to fail, and failure has a hard ceiling: one revision surgery, then amputation. Nobody in the industry had framed it as a materials problem until Jain's partner did. That's now the thesis behind a portfolio company's first non-metallic implant.

"Our secret sauce is not the deals," Jain says. "It's understanding this space so well that nobody can tell us something we don't believe has happened to be true." That bar isn't built by researching a sector for six months. It has to be earned elsewhere first, and the fund gets built around it, not the reverse.

Would You Trust This Partner If a Deal Went Wrong?

Malynur raised the topic; fund managers ask him constantly what to look for in a partner. Jain's answer wasn't about sourcing. It was about who you're doing it with.

"Partnerships fail in this business, never because you couldn't raise capital." They fail because the partnership was an afterthought, "a marriage of convenience," formed because everyone else was raising a fund. His metaphor: a fund partnership is a marriage, except investors are the children. Getting in is easy, it just takes money. Getting out, when the fit is wrong, is far harder for people who aren't the partners.

His real test isn't chemistry. It's whether you've seen the other person under real stress, finger-pointing or solving the problem, because something will eventually go wrong. Diligence this before capital, not after: Do the skills actually complement each other? Who owns investor relations, sourcing, and underwriting? Do you trust each other enough to protect investors before your own ego?

How Do You Keep the Fund Funded Between Raises?

That was the question Malynur asked directly: how does Scalpel handle fund expenses when the underlying investments aren't cash-flowing? Pre-revenue funds face a specific problem: no cash flow to fund accounting, compliance, or the manager's time. Working with Avestor's legal and platform advisors, Scalpel built its fix: 20% of contributed capital held in reserve, split evenly between management fee and expenses.

On a $100,000 check, $80,000 goes into the deal; fees stop after five years, unused reserve returns to investors.

The percentages aren't the point; they were reverse-engineered from actual costs, not copied. A real estate fund with rental income has different options entirely: due diligence fees, promote share, preferred distributions, because the deal itself already generates cash. Economics have to match the strategy's cash-flow reality, not whatever the last manager used.

Should You Take Every Investor Who Wants In?

Malynur asked Jain where Scalpel finds its investors, expecting, perhaps, a marketing answer. Jain's investor base grew by referral and track record, and he's turned money away on purpose. His filter is fit, not check size.

One prospective investor wanted to put in $25,000, missed the deadline, then spent thirty hours across follow-ups signaling he was looking for certainty venture investing can't provide. Jain told him directly the fit was wrong. That conversation eventually led to the same investor putting in $700,000, on his own terms, not under pressure. An investor who needs certainty a strategy can't offer doesn't get less demanding after wiring money. Saying yes to the wrong one costs more than saying no.

What's Your Actual Track Record, Not the One You're Pitching?

Sixteen years pre-fund: minimum return 3x, max 27x, no capital lost. Since formalizing in 2023: one full exit at 7x, one 3x distribution without exiting, one company likely public this year, another a likely acquisition by 2027. That is Saket's track record.

Jain won't call this a win rate. Nothing's been realized as a loss, but nothing's completed a full cycle either. "We can't say the win rate is..." He stops short deliberately. That restraint is rare in fundraising materials, and worth noting.

One layer underneath: Qualified Small Business Stock can exempt up to $10 million in gains on qualifying holdings of three to five years. Scalpel spent roughly $25,000 in legal fees understanding exactly how it applies. Tax treatment on an exit isn't a detail to sort out later; paired with a real track record, it's part of the pitch itself.

Is Your Structure Ready Before the Deal Is?

None of this was assembled reactively. As Avestor co-founder Badri Malynur puts it: you don't want to start digging the well when the fire is already burning. Once the structure exists, a manager moves fast when a real opportunity appears. Without it, the most important weeks get spent on paperwork instead of diligence.

What must exist before the first deal:

- Fund structure and exemption strategy, reviewed with counsel

- Legal documents ready to execute

- Onboarding, accreditation, KYC/AML workflows built

- Reporting cadence and expense model defined in advance

- Tax treatment understood before the first close

- Partner roles clarified before a disagreement forces the issue

None of them guarantee a good deal. It guarantees the manager isn't the bottleneck when one appears.

What Happens After the Fund Launches?

A fund isn't proven when the documents are executed. It's tested when the second deal appears, and the structure either holds or doesn't, when an investor pushes back on the expense model, when a partnership hits real disagreement instead of a hypothetical one.

Raising capital, even though it's hard, isn't that hard if it's done properly. It takes time. It doesn't reward shortcuts. The managers still standing after the fifth raise treated the structure as seriously as the deal.

The deal gets the attention. The structure decides whether there's a second one.

Where Avestor Fits Into Scalpel's Story

None of Scalpel's structure was built alone. Jain worked directly with Avestor to stand up the Customizable Fund® model that let Scalpel offer deal-by-deal investor choice without a new entity and a new legal bill every time. When one of Scalpel's investments produced a distribution instead of a clean exit, a situation with no obvious playbook, Jain didn't call around for an outside advisor. He got Avestor's co-founders on a call and resolved it the same day.

That's the part Jain kept returning to on the webinar: the platform isn't just documents and a portal. It's the same team on the other end of the phone when something in a live deal doesn't fit the template.

His advice to any manager considering this path was blunt: raising capital isn't as hard as people think, if the structure is built properly and built early. Talk to the team before the deal creates the urgency.

If you're building a fund and want to see how the Customizable Fund® model could work for your strategy, book a call with Avestor.